EAF steelmaking economics 2019.

Electric Arc Furnace Steelmaking Costs 2019.

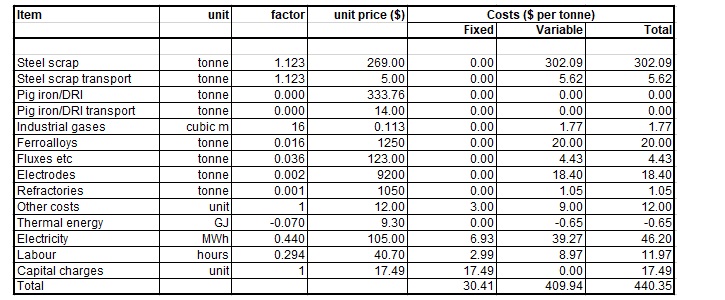

Conversion costs for electric arc steelmaking

Steel Cost Modelling Notes

The Steel Costing ModelThe economic model shown above is prepared only to shown how liquid steel cost can be calculated through a simple cost benchmarking type approach. The predicted total costing shown is not meant to represent an actual cost for any real steel company. It is a notional figure only - albeit one that is built on fairly representative current input costing information.

Input CostsKey input costs are taken from the other pages shown on the steelonthenet.com website or estimated by our economists. Recent scrap and electricity prices can be found on our steelmaking input costs page. Analysis above was prepared in July 2019.

The Steel ProductThe steel product for which the cost is shown above is a metric tonne of EAF liquid steel. The cost is for a notional producer - a typical size plant of about 1m t/year capacity, based in Japan, using a 100% scrap charge to EAF [no DRI or irons], and producing commodity grade carbon steel for long products with average labour productivity. To benchmark or estimate conversion costs for different locations, for steel grades such as stainless steel, or for specific producers please contact us (see below). Steel costs for the integrated steelmaking process route may be found on our BOF costs page.

The Business EnvironmentSite visitors are advised that all estimates shown should be adjusted to reflect the particular business environment in which the steel plant operates. Thus, electricity charges may be substantially cheaper than usual because the melt shop is run primarily at night (to benefit from cheaper night time tarrifs). Depreciation costs may be higher or lower depending on the age of the electric furnace and transformer. Labour productivity may also be substantially poorer than shown (especially in State owned plants prior to privatisation) etc.

Accounting MethodsActual cost estimates can also differ due to local accounting policies and practices. The figures above for example assume straight line depreciation over a 20 year asset lifetime. The estimates also assume that 25% of labour cost are fixed - whilst in practice, all costs will be variable over the longer term. The model above endeavours to present the economic data on the basis of standard management accounting practices - users of the model should however be clear that the model is likely to require adaptation for different accounting circumstances.

Cost UpdatesTo estimate the impact of a change in any main input (scrap, ore, other steel raw materials, energy, or labour) on the total, fixed or variable production costs of any steel product (semi-finished; or flat, long, or pipe and tube finished steel products) made through either main production process route (integrated steel manufacturing or electric arc steelmaking), please email info@steelonthenet.com for assistance.

To contact us about this steelmaking cost economics page please email info@steelonthenet.com.